Whether you need medical care while traveling, in the comfort of home, or you want the flexibility to see any medical doctor or specialist that accepts Medicare, a Medicare Supplement plan may be just what you need. As you prepare for the next chapter of your journey,...

By Ian Berger, JD IRA Analyst In the July 22, 2024 Slott Report, my colleague Sarah Brenner explained how the IRS, in its final SECURE Act required minimum distribution (RMD) regulations issued on July 18, did not budge on a controversial position it had taken in its...

Navigating retirement can be overwhelming given uncertainties like market volatility, inflation, life expectancy and the state of Social Security. Like having a mechanic give your car a periodic once-over, regularly reviewing your spending and saving can help keep...

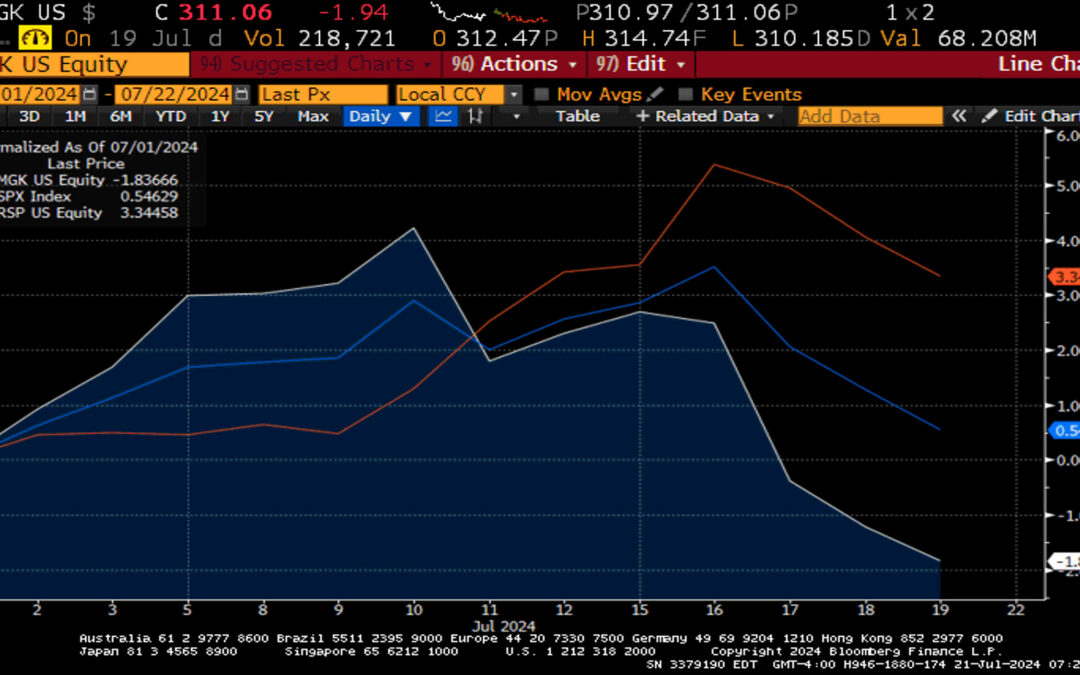

It was a very busy week on Wall Street as investors seemed inclined to rotate out of Mega-cap tech and into this year’s laggards. A failed assassination attempt on former President Donald Trump last Saturday in Pennsylvania only bolstered his chances for reelection...

It was a very busy week on Wall Street as investors seemed inclined to rotate out of Mega-cap tech and into this year’s laggards. A failed assassination attempt on former President Donald Trump last Saturday in Pennsylvania only bolstered his chances for reelection...

By Ian Berger, JD IRA Analyst Question: One of our clients wants to cash out his IRA and then roll it into a Roth IRA within 60 days. Can this be done directly, or does it have to be rolled back into an IRA first and then converted? Thanks, Samuel Answer: Hi Samuel, A...

The benefits of Medicare are initially activated when you turn 65. That is when you first enroll in this federal healthcare program for seniors. But what if you are still working at the age of 65 and don’t want to officially retire? Medicare enrollment and retirement...

KEY POINTS An improving economy has helped modestly improve the outlook for Social Security’s funds. But experts say the outlook for the program still points to the need for imminent reform. A new Social Security trustees report released Monday provides a modest...

By Andy Ives, CFP®, AIF® IRA Analyst When an IRA owner does a Roth conversion, there is typically a 5-year clock for the earnings on the converted dollars to be tax free. If a person already had a Roth IRA for 5 years AND is over 59 ½, there is no conversion...

By Ian Berger, JD IRA Analyst One of the more interesting rules (if any could be called “interesting”) from the 2022 IRS proposed regulations requires spouse beneficiaries in some situations to take RMDs (required minimum distributions) before doing a spousal...

By Andy Ives, CFP®, AIF® IRA Analyst QUESTION: Do required minimum distributions (RMDs) need to be taken when a non-spouse beneficiary inherits Roth IRA? It seems this has been a point of confusion for some time. ANSWER: This is something that confuses a lot of...

Whether you are already part of the nearly 60 million enrollees of the program, or are looking to join its ranks soon, we are here to help you answer the most commonly asked question – how to choose the right Medicare plan for you. Before you apply for Medicare, it is...

KEY POINTS From now until 2030, 30.4 million Americans are expected to turn 65. Women who are entering retirement now face more financial risks than their male counterparts, new research finds. The largest cohort of baby boomers is poised to reach age 65 between now...

By Sarah Brenner, JD Director of Retirement Education If you are charitably inclined and have an IRA, a Qualified Charitable Distribution (QCD) can be a great strategy. With a QCD, you can move IRA funds to the charity of your choice tax-free. Here are 12 QCD rules...

By Andy Ives, CFP®, AIF® IRA Analyst If I pour too much water into a glass, removing liquid from a different glass does not correct the problem. The excess water must be removed from the “offending” receptacle. Such is the case with excess IRA contributions. If too...

Planning for retirement is hard for many reasons, including the challenge of answering one key question: Just how long will I be retired? Knowing how much time you’ll have to enjoy your golden years is paramount to budgeting; after all, you can’t determine how much...

To help bring clarity, we have compiled a “New to Medicare” checklist to help you out with all the basic Medicare information that you’ll need. Before 1965, Americans over the age of 65 had difficulty gaining access to private health insurance coverage....

-Darren Leavitt, CFA The holiday-shortened week saw the S&P 500 hit its 34th record high this year. The NASDAQ 100 also eclipsed the 20k mark for the first time. Traders welcomed weaker-than-expected economic data that fostered the likelihood that the Federal...

By Ian Berger, JD IRA Analyst If you take a taxable withdrawal from your IRA or 401(k) (or other company plan) before age 59 ½, you normally have to pay a 10% penalty in addition to taxes. But Congress continues to carve out exceptions to this penalty, and there are...

By Sarah Brenner, JD Director of Retirement Education More and more Americans have retirement savings in Roth 401(k)s. With their rising popularity come some complicated tax issues. These funds are often rolled over to Roth IRAs at retirement or when a...